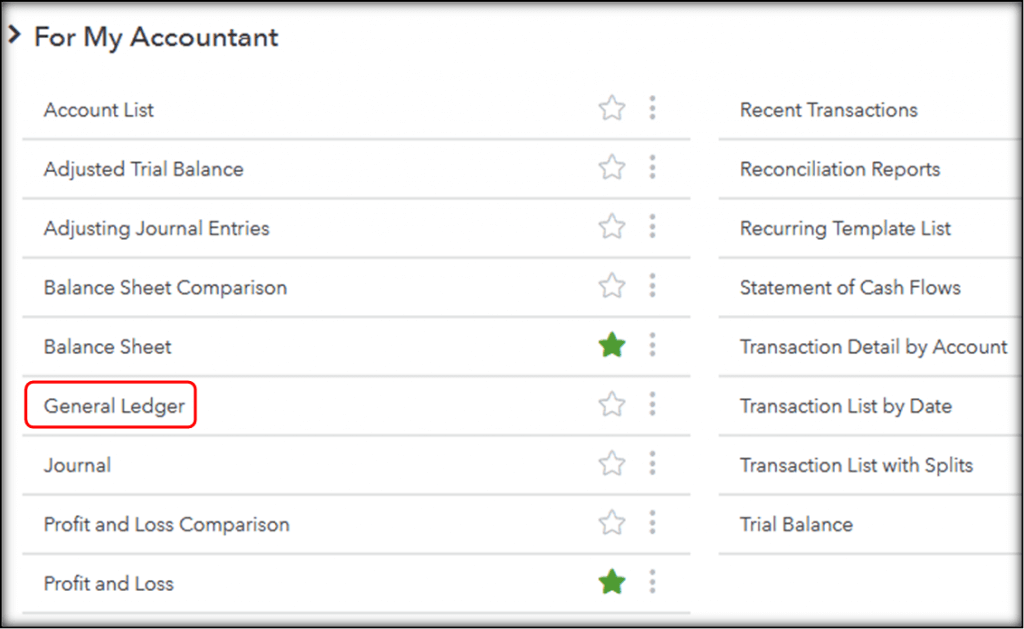

How to view general ledger in QuickBooks

We used to do all of our accounting by hand before computers and apps. Accouavailablenting documents were stored in massive binders with reams of paper files by business owners. Fortunately, accounting has gone digital, and as a small business owner, you can use accounting software like QuickBooks to automate your financial transactions.

Income statements, balance sheets, and cash flow statements are examples of financial statements that indicate a company’s financial health. The accounting period, which involves the general ledger, can be used to produce all three claims. There are four stages in the accounting cycle:

- Compile a list of sources: Source records such as receipts and invoices are used to post transactions. To post a journal entry, each accounting document is used.

- Make entries in your book: An account number, a date, a dollar sum, and a summary of the submission are included in a journal entry. Accountants can post data to monitor accounts before transferring it to a journal entry in some cases.

- Make entries in the general ledger: The journal entries make their way through the general ledger. Although some small companies use Excel to keep track of their public ledger accounting, accounting software is a more effective.

- Produce financial reports: The accountant creates a trial balance that lists each account and its current balance to prepare the financial statements. Financial reports can be generated using a modified trial balance.

The general ledger is a company’s primary accounting record in financial accounting. Although there are tools that automatically categorise these transactions, understanding the fundamental components of general ledger accounts is still essential. You will find possible problems with your financial data if you know the details.

What is the concept of a general ledger?

A general ledger is a method for sorting, storing, and analysing a company’s financial transactions. A journal entry, a summary, debit and credit columns, and a balance are the four main components of a general ledger:

- A journal entry: A journal entry consists of the number and date of each journal entry posted to the account.

- A description: A summary of the transaction is given.

- Debit and credit columns: Each journal entry posts a debit or credit to the general ledger in the debit and credit columns.

- A balance: When a debit or credit is posted to an account, the account balance is listed in the general ledger. The ending ratio is determined at the end of the month after all of the journal entries have been posted.

The trial balance can be produced using the account balances in the general ledger. Any account and the current account balance are listed in a trial balance. In a double-entry accounting scheme, the dollar amount of total debits would equal the dollar amount of full credits. There are five types of accounts in the general ledger. The income statement reports two sections, while the balance sheet uses three (assets, liabilities, and equity) (revenue and expenses).

Assets, liabilities, equity, sales, and expenditures are the different types of general ledger accounts. The map of accounts is also mentioned in the general ledger.

- Possessions: Assets are monetary-valued tools that companies use to produce revenue. An asset may be tangible (i.e., a piece of equipment) or intangible (i.e., a piece of property) (copyright). Cash, inventory, land, trademarks, and patents are examples of assets.

- Obligations: Liabilities are debts that a company owes to another company or entity. Employee payroll, bank loans, mortgages, and leases are also examples of liabilities.

- Equity: The difference between total assets and total liabilities is known as equity. Any capital left over after a company sells all of its properties for cash and pays off all of its debts is equity. The equity balance is made up of three parts:

- Stock that is traded on a regular basis: The common stock balance is the number of shares issued multiplied by the stock’s par value if the company issues stock to investors. Par value is usually $1 or $5 per share.

- Additional money that has been paid in: This is the price paid by investors for common stock in excess of its par value. If a stock with a par value of $1 is worth $10 per share, $9 per share is added to the additional paid-in capital.

- Earnings that are held: A company may opt to pay a dividend to shareholders or keep profits to use in the business. The retained earnings balance is calculated by subtracting total business earnings from total dividends paid to shareholders since the company’s inception. Instead of common stock, small companies that do not issue stock have an account called owner’s equity. The cumulative cash and other assets contributed by the owners make up the owner’s equity.

- Earnings: The selling of a product or service produces revenue. Sales, interest income, dividends, and all other fees collected by the company are all considered revenue.

- Charges:To generate sales, a company must incur expenses. Typical company expenditures include rent and electricity.

Conclusion

In conclusion, QuickBoooks Desktop software is an accounting software that has always been regarded by different categories of bookkeepers and accountants. The motive of this blog is to help you understand the importance of general ledger in QuickBooks accounting software. I hope that this blog helps you and was worth your time.